The most sophisticated investors in the world are allocating more of their assets to Alternative Investments due to chronically low bond yields, extreme central bank intervention, and the threat of overheated stock valuations. They believe that Alternative Investments will give them a better chance of achieving sufficiently higher returns to meet future obligations while protecting against excessive downside risk.

Goodbye Traditional 60%/40% Portfolio – High-interest rates during the 80’s and 90’s supported the case of the “balanced” portfolio. Today, volatile equity markets coupled with increasing interest rates and low return bonds have created headwinds for the investment community.

Barrons, JP Morgan, and Bank of America all say your traditional 60/40 retirement portfolio is dead. In fact, JP Morgan says your 60% equity and 40% fixed income portfolio will only be expected to generate 3.2% annually going forward. For the majority of Canadians, 3.2% after inflation and taxes simply will not work!

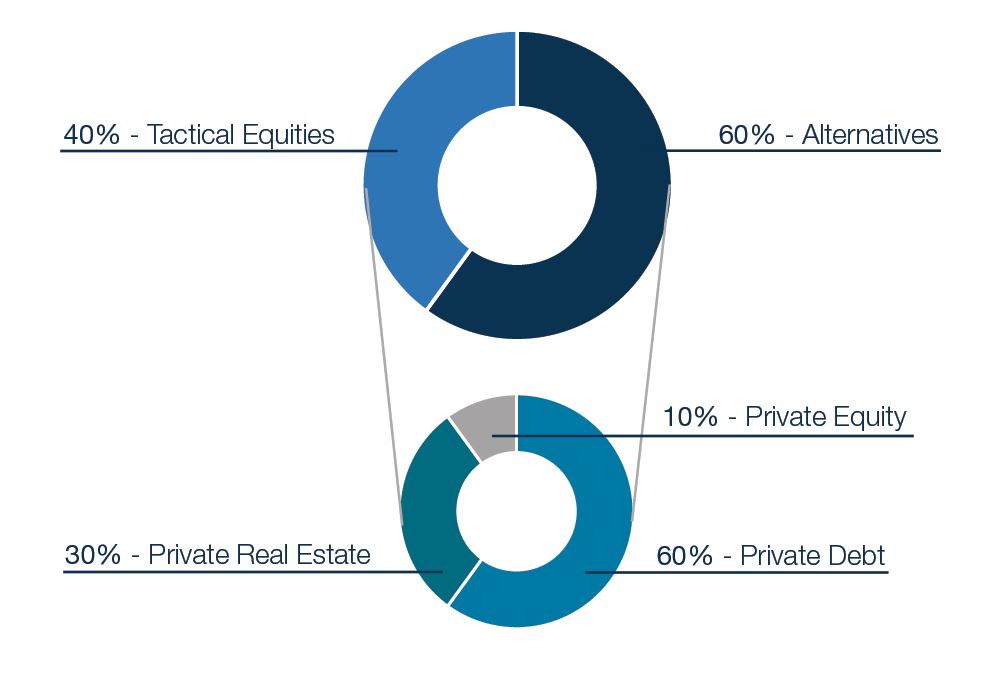

Hello New Pension Fund Style 60% / 40% Portfolio – At Harbourfront, we believe an asset mix (as shown here) 40% Tactical Equities, 60% Alternatives.

")

Strategic Private Wealth Counsel. Embodying a philosophy of independent, unbiased advice with an unwavering commitment to delivering true wealth management.

© 2025. Copyright by Strategic Private Wealth Counsel of Harbourfront Wealth Management Inc. All Rights Reserved. No portion of this site may be replicated without permission.